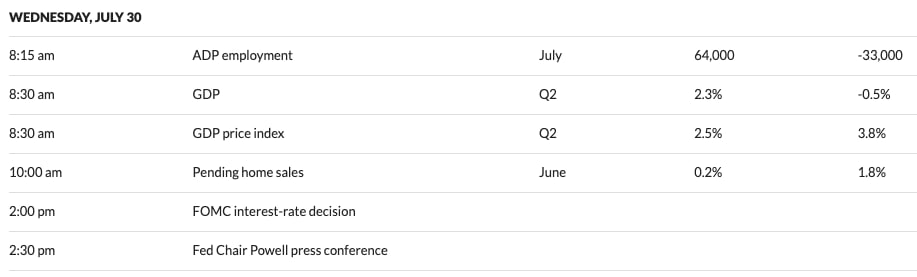

With the Federal Reserve’s interest rate decision just hours away, key U.S. economic data released this morning has set the tone: both employment and GDP growth came in stronger than expected.

According to ADP, the U.S. economy added 64,000 private-sector jobs in July, rebounding sharply from the 33,000 job decline seen in June. While still below long-term averages, the reversal eases some concerns of a potential labor market cooldown.

At the same time, the second-quarter GDP rose 2.3%, a sharp recovery from the 0.5% contraction in Q1. The GDP price index, a key measure of inflation embedded in economic output, printed at 2.5%, also showing a significant slowdown from 3.8% in the previous quarter.

Housing data added nuance to the picture. Pending home sales rose by just 0.2% in June a steep drop from May’s 1.8%, reinforcing that the real estate market remains sensitive to current interest rate levels.

All eyes now turn to the FOMC decision at 2:00 PM ET, where the Fed is widely expected to hold rates steady. However, the tone of Chair Jerome Powell’s press conference at 2:30 PM ET will be crucial in shaping expectations for a potential rate cut in the coming months.

Markets are split on whether the Fed will initiate cuts as early as September or wait for further confirmation of disinflation. Today’s stronger-than-expected data may give policymakers reason to delay easing, but much will depend on Powell’s tone regarding future risks and inflation trajectories.

source: ADP, U.S. Bureau of Economic Analysis, National Association of Realtors, Federal Reserve